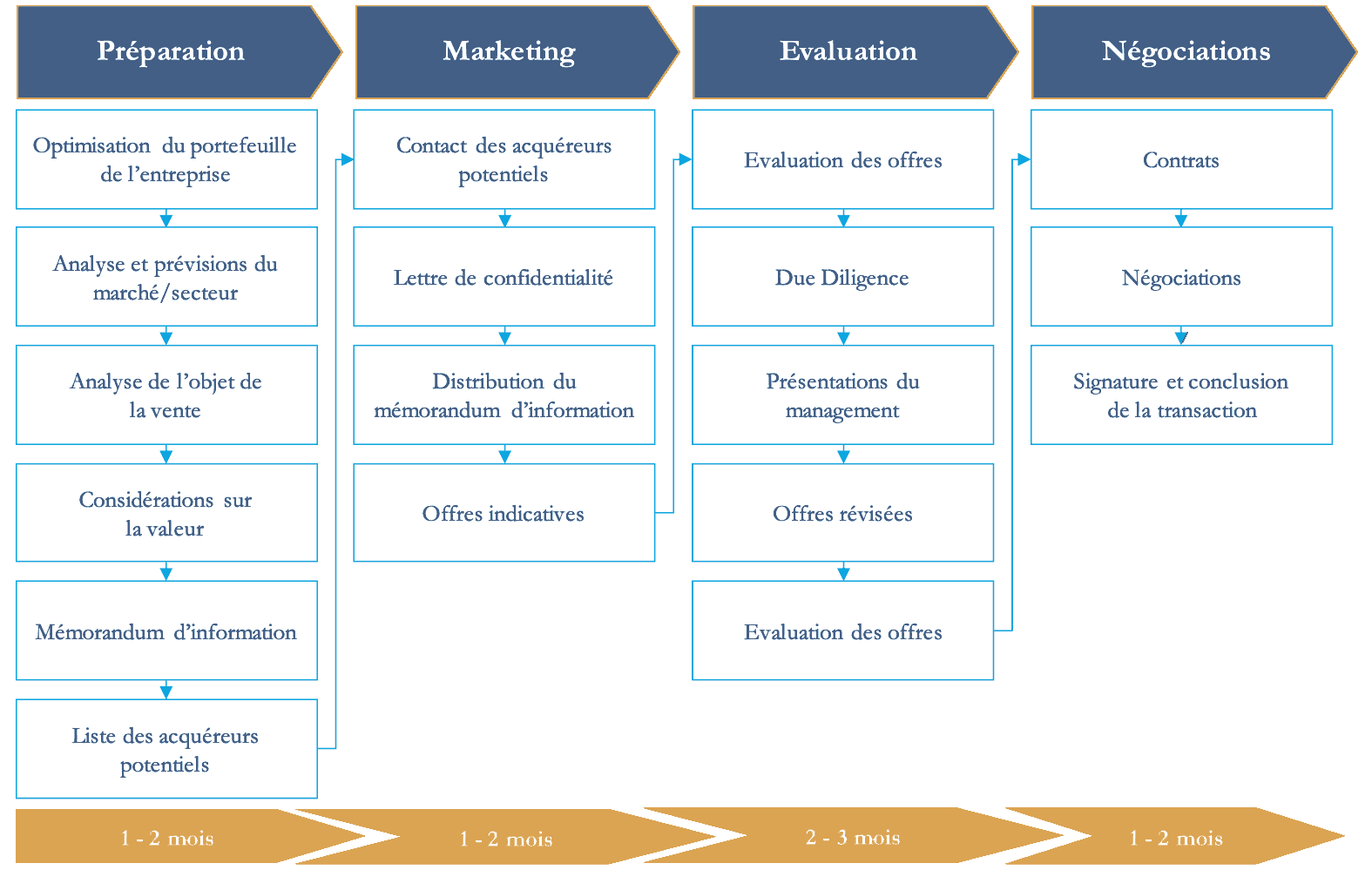

A sales process is essentially divided into four phases that may overlap.

The sales documentation and the list of potential buyers are prepared with the client during the "Preparation" phase. The "Marketing" phase is the approach of the parties, first of all anonymously, followed by the distribution of the information memorandum to the parties who have signed a confidentiality agreement. The receipt of indicative offers, an in-depth discussion session with certain parties and the opening of a data room accessible to buyers constitute the "Evaluation" phase. Finally, the "Negotiations", with one or more parties, of the main terms of the agreement and then detailed elements until the signature with the buyer of a purchase/sale contract. Such a process typically takes 6 to 9 months, but can be lengthened depending on the circumstances.

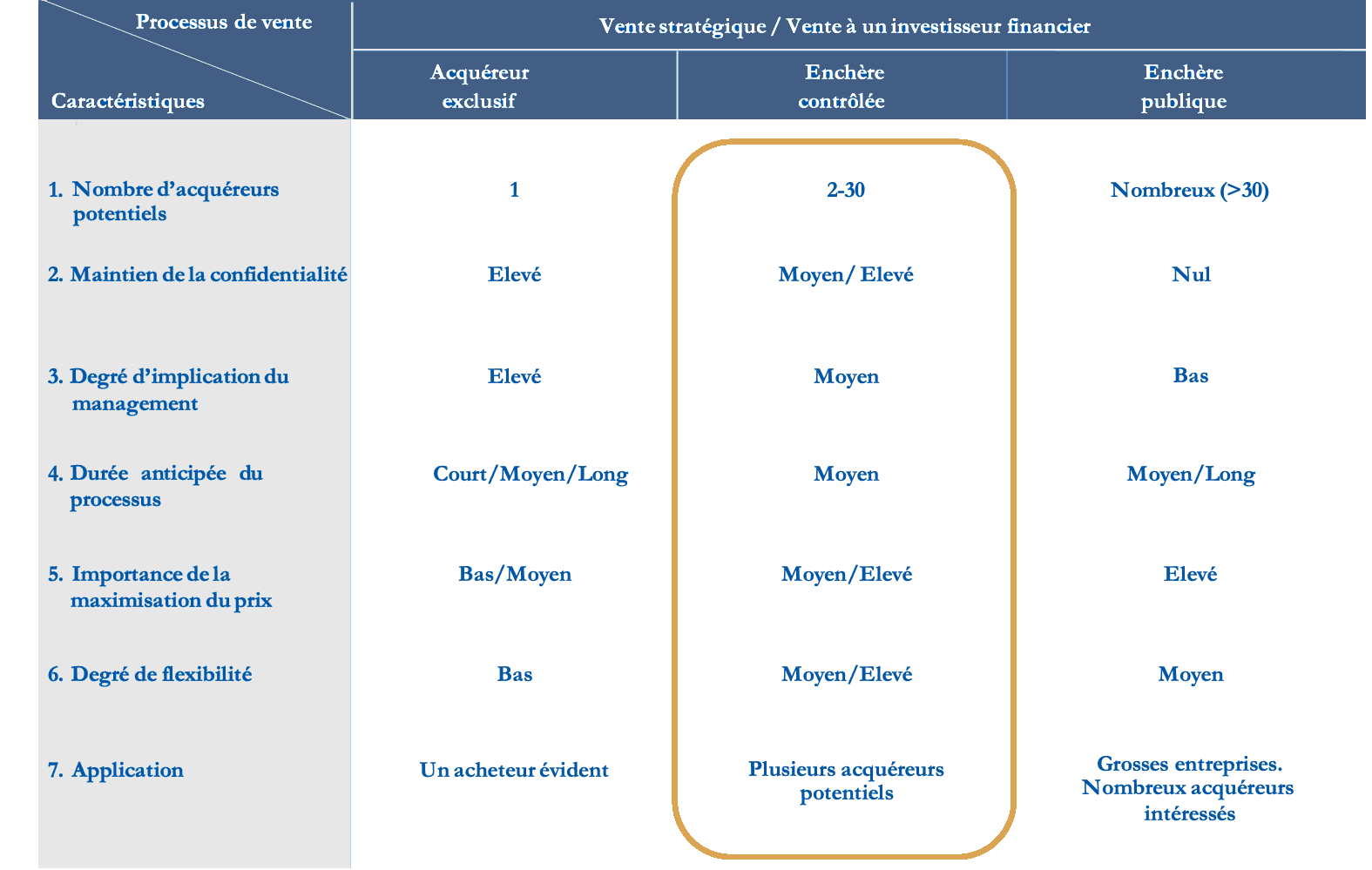

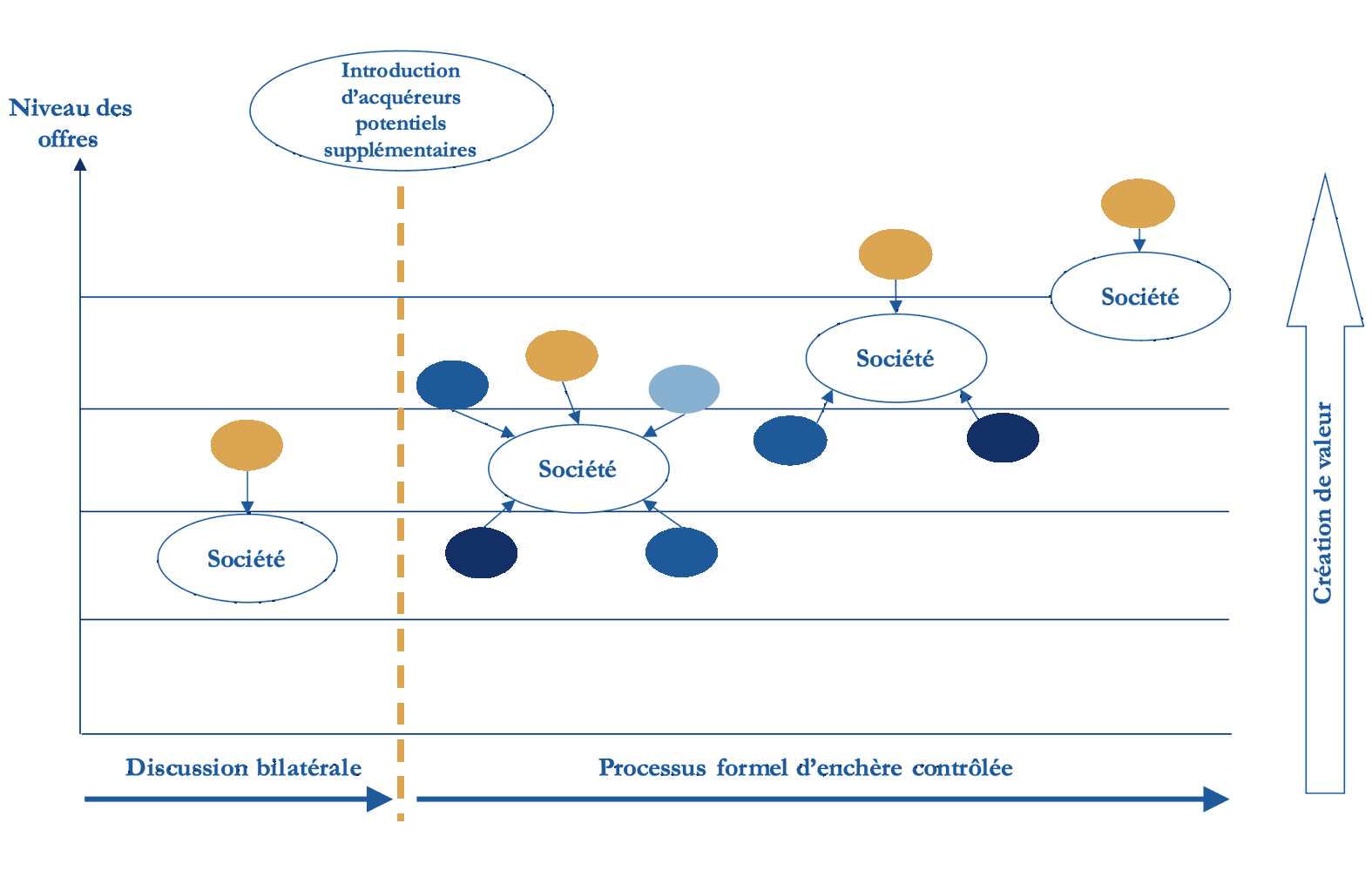

A controlled auction process combines the best of both worlds: the confidentiality of an exclusive process between two parties on the one hand, and the competition that is stimulated in public auctions on the other. This means introducing competition to maximize price, while maintaining confidentiality so as not to disrupt the company and its ecosystem during the sales process. Only an M&A advisor can manage a process of such intensity where interactions with multiple counterparties take place in parallel and simultaneously.